1. Traditional ways of raising capital

Two major ways to raise equity for private firms

- 1.1 Brief note on Venture Capital (VC)

Unlisted firms have different options to raise equity

Equity financing over the firm's life cycle

| Unlisted firms | Listed firms |

| - Angel investors - Venture Capital - Institutional investors - Corporate investors - IPO |

- Private placement (to small group of investors) - Right issue (to existing shareholders) - Dividend reinvestment plan (Instead of div.get shares) |

VC provides diversification and expertise at a high cost

Benefits & Costs of VC

Venture capital firm = limited partnership, specialized in raising capital to invest in young firms.

| Benefits for VC limited partners vs. Angel investors | Costs: |

| - More diversification & Expertise of general partners. | - 2% management fee of committed capital. - 20% of positive returns. |

사기업들이 자본을 조달하는 두 가지 주요 방법 중 하나는 벤쳐 캐피탈 (VC).

벤처 캐피탈은 투자 전문성과 다양성을 제공하지만 높은 비용이 든다.

벤처 캐피탈 회사는 주로 limited partnership 구조를 갖추고 있으며,

주로 젊은 회사에 투자하기 위해 자본을 모으는데 전문화 되어있다.

벤처 캐피탈의 이점과 비용:

- 이점

- 다양성: 벤처 캐피탈은 여러 회사에 투자함으로써 투자 위험을 분산시킬 수 있습니다.

- 전문성: 벤처 캐피탈의 일반 파트너들은 투자와 관련된 전문 지식을 가지고 있어, 투자할 회사를 선택, 관리하는 데 큰 도움

- 비용

- 관리 비용: 벤처 캐피탈은 투자자로부터 받는 총 약정 자본의 2%를 관리 수수료로 받습니다.

- 성과 수수료: 투자로 발생하는 수익이 긍정적일 경우, 그 수익의 20%를 성과 수수료로 받습니다.

벤처 캐피탈이 제공하는 다양성과 전문성은 투자 리스크를 관리하고 수익성 있는 기회를 찾는데 큰 장점이 되지만, 그 대가로 관리 및 성과 수수료가 발생하게 됩니다. 따라서 투자 결정을 내릴 때 이러한 비용을 고려해야 합니다.

The post-money valuation is the valuation after a funding round

Example: Venture valuation

Votek, a UAE start-up working on Arabic speech recognition software, needs additional capital. Assume that, initially, the founder invested $800,000 and received 8 million shares of stock. Votek now needs to raise a second round of capital (series A funding), and it has identified an interested venture capitalist. This venture capitalist will invest $1 million and wants to own 20% of the company after the investment is completed.

Q1)

How many shares must the venture capitalist receive to end up with 20% of the company?

What is the implied price per share of this funding round?

A1)

8,000,000 = 0.80 × TOTAL -> TOTAL = 10m shares.

- VC will own 2m shares. (10m-8m).

- Paid $1m for the shares.

- New (implied) share price: $0.50.

Q2) What will the value of the whole firm be after this investment, i.e. the value of the whole firm (old plus new shares) at the price the new equity is sold at (the post-money valuation)?

A2)

Post-money valuation:

10m shares × $0.50 = $5m.

Good deal for the founder?

The valuation wise, it's good. But, ownership is diluted. (Trade-off should be considered).

Votek이라는 회사가 더 많은 돈이 필요해서 벤처 캐피탈리스트에게 돈을 받기로 했습니다. 이 벤처 캐피탈리스트는 $100만을 투자하고 투자 후에 회사의 20%를 소유하길 원합니다.

- 주식 수와 주당 가격 계산하기

- Votek에는 이미 800만 주가 있습니다.

- 벤처 캐피탈리스트가 회사의 20%를 차지하려면, 전체 주식 수는 1000만 주가 되어야 합니다.

- 따라서 벤처 캐피탈리스트는 200만 주를 새로 받습니다.

- 이 200만 주를 위해 $100만을 지불했으므로, 계산상 각 주의 가격은 $0.50입니다.

- 회사의 총 가치 계산하기

- 새로운 주식 가격인 $0.50을 기준으로 전체 주식을 계산하면, 회사의 총 가치는 $500만이 됩니다.

간단히 말해서, 이 투자로 인해 Votek의 전체 가치는 $500만으로 평가되고 있습니다. 이는 벤처 캐피탈리스트가 투자한 금액과 회사에서 차지하는 지분율을 고려했을 때 산출된 값입니다. 이런 상황에서 창업자가 이 거래로부터 이익을 보는지 여부는, 추가 자본이 회사를 얼마나 성장시킬 수 있는지에 달려있습니다.

투자 전 기업 가치는 프리머니 밸류(Pre-Money Valuation), 투자 후 기업가치는 포스트머니 밸류(Post-Money Valuation)라고 해요. 쉽게 말해 프리머니 밸류에 투자금을 더하면 포스트머니 밸류.

- 1.2 Initial Public Offerings (IPOs)

IPO offer price can be determined by fixed price offer

Fixed price offer:

| 정의 | 리스크 |

| Price is set, prospectus sent out, and offers are received. | 1. Price too high: Uncertainty for the issuer 2. Price too low: Money "left on the table" 3. Underwriting costs? |

Book-Buiding:

| Open pricing | Constrained open pricing |

| 1. Bids taken from market 2. The final price is a clearing price that issues all shares. |

1. Investors are invited to bid for shares within the predetermined price range 2. Final issue price determined by the level of investor demand -> lets market forces establish the equilibrium price. |

초기 공개 제공(IPO)과 고정 가격 제안

IPO, 즉 기업공개는 기업이 주식을 공개 시장에 처음으로 판매하는 과정입니다.

IPO의 발행 가격은 '고정 가격 제안' 방식을 통해 결정될 수 있습니다.

- 고정 가격 제안

- 정의: 발행가격을 미리 정하고, 그 가격을 투자 설명서에 명시한 뒤 투자자들로부터 주문을 받습니다.

- 리스크:

- 가격이 너무 높을 경우: 발행자에게 불확실성을 초래하며, 주식이 팔리지 않을 수 있습니다.

- 가격이 너무 낮을 경우: 발행자가 더 많은 자금을 조달할 수 있었음에도 불구하고 자금을 놓치는 상황이 발생할 수 있습니다.

- 발행 비용: IPO 과정에서는 발행을 돕는 금융기관의 수수료 등 다양한 비용이 발생할 수 있습니다.

- 북빌딩 방식

- 개방형 가격 설정과 제한적 개방형 가격 설정:

- 개방형 가격 설정: 시장에서 입찰을 받아 최종 가격을 결정합니다. 이 가격은 모든 주식을 발행할 수 있는 청산 가격이 됩니다.

- 제한적 개방형 가격 설정: 투자자들이 미리 정해진 가격 범위 내에서 주식을 입찰할 수 있도록 초대합니다. 최종 발행 가격은 투자자 수요에 따라 결정되며, 시장의 힘에 의해 균형 가격이 설정됩니다.

- 개방형 가격 설정과 제한적 개방형 가격 설정:

이 두 가지 방식은 IPO를 진행할 때 기업이 선택할 수 있는 대표적인 가격 결정 방법입니다. 각 방식은 장단점이 있으며, 기업의 상황과 시장 조건에 따라 적합한 방법을 선택해야 합니다.

One rare way to price IPOs is through an auction

Example open pricing: Auction IPO

• Underwriter in auction IPO takes bids from investors and then sets the price that clears the market.

• Example: Google

- IPO 08/2004.

- Dutch auction process.

- On the first trading day, shares were up 18% closing at $100.34.

- Shares were underpriced.

경매를 통한 IPO 가격 결정 방법

IPO에서 드물게 사용되는 가격 결정 방법 중 하나는 경매를 통한 방법입니다. 이는 기업이 주식을 공개적으로 경매에 부치고, 투자자들이 입찰을 통해 가격을 결정하는 방식입니다.

경매 IPO의 예로 구글의 경우를 들 수 있습니다. 구글은 2004년 8월에 IPO를 진행했으며, 네덜란드식 경매 방식을 사용했습니다. 첫 거래일에 구글의 주식은 발행 가격보다 18% 상승하여 $100.34에 마감했습니다. 이는 주식이 저평가되었음을 의미합니다.

The auction underwriter takes bids directly from investors

IPO auction – Example

• Ashton, Inc., is selling 900,000 shares of stock in an auction IPO.

• At the end of the bidding period, Ashton’s investment bank has received the following bids:

| Price ($) | Number of Shares Bid |

| $10.00 | 175,000 |

| $9.75 | 200,000 |

| $9.50 | 275,000 |

| $9.25 $9.00 |

275,000 300,000 |

What will be the offer price of the shares?

경매 방식 IPO 예시: Ashton, Inc.

Ashton, Inc.는 900,000주의 주식을 경매 IPO를 통해 판매하고 있습니다. 입찰 기간이 끝난 후, Ashton의 투자은행은 다음과 같은 입찰을 받았습니다:

- $10.00에 175,000주

- $9.75에 200,000주

- $9.50에 275,000주

- $9.25

- $9.00에 275,000주, 300,000주

The IPO price is the auction price that clears the supply of shares

(how clearing price works)

IPO auction – Solution

• The winning auction price would be $9.25.

| Price | Cumulative demand |

| $10.00 $9.75 $9.50 $9.25 $9.00 |

175,000 375,000 650,000 925,000 1,225,000 |

여기서 IPO 가격은 주식 공급을 청산할 수 있는 경매 가격입니다.

입찰을 통해 받은 주문을 누적하여

가장 낮은 가격에서 공급량(900,000주)을 충족시킬 수 있는 가격을 찾습니다.

- $10.00에서 누적 수요: 175,000주

- $9.75에서 누적 수요: 375,000주

- $9.50에서 누적 수요: 650,000주

- $9.25에서 누적 수요: 925,000주

- $9.00에서 누적 수요: 1,225,000주

따라서, 900,000주를 청산할 수 있는 최초의 가격은 $9.25입니다.

이 가격이 Ashton, Inc.의 IPO에서 제시된 주식의 발행 가격이 됩니다.

The underwriter guarantees the success of the issue

Role of the underwriter in the capital raising process

- The principal role is to guarantee the success of the issue.

- 2 Types: "Firm Commitment" vs. "Best Efforts".

- Fulfils insurance function:

- Underwriter bears risk if the issue is not fully subscribed.

- Underwriting risk = risk of a shortfall. - Other roles of underwriter include:

- Recommend issuing method + value securities - - Underwriters are investment banks and stock broking firms.

- Underwriter costs at high and not very sensitive

- A typical spread is 7% of the issue price.

발행 보증인의 역할은 자본 조달 과정에서 발행의 성공을 보장하는 것입니다. 이는 기업이 자본 시장에서 자금을 조달할 때 중요한 역할을 담당합니다. 보증인은 주로 투자은행이나 증권 중개 회사들이 맡게 됩니다.

발행 보증의 두 가지 유형

- 확정 계약(Firm Commitment)

- 보증인이 발행되는 증권을 직접 구매하여 재판매합니다.

- 만약 증권이 전부 팔리지 않는 경우, 보증인이 그 위험을 부담합니다.

이러한 위험을 '발행 위험' 또는 '부족 위험'이라고 합니다.

- 노력에 의한 계약(Best Efforts)

- 보증인은 증권을 판매하려 최선을 다하지만, 모든 증권이 팔리지 않더라도 보증인이 위험을 직접 부담하지는 않습니다.

- 이 방식은 발행인에게 더 높은 리스크를 줄 수 있습니다.

발행 보증인의 기타 역할

- 증권 발행 방식과 가치 평가에 대해 권고합니다.

- 발행 과정에서 마케팅 및 판매 전략을 조언하고 수행합니다.

발행 보증인의 비용

- 보증인의 서비스 비용은 일반적으로 발행 가격의 7% 정도의 스프레드로 설정됩니다.

- 이 비용은 발행 보증인이 감수하는 위험과 수행하는 역할에 비해 고정적이며,

시장 상황에 따라 크게 변하지 않는 경향이 있습니다.

이렇게 발행 보증인은 자본 조달 과정에서 중요한 안전망 역할을 하며,

기업이 자본 시장에서 필요한 자금을 효과적으로 조달할 수 있도록 돕습니다.

Underwriter costs are high and not very sensitive.

A typical spread is 7% of the issue price.

- Seems large given that there is also underpricing.

2. Brief history of crowdfunding

Internet crowdfunding allegedly started in 1997.

First examples of internet crowdfunding:

• 1997: British rock band Marillion.

- US fan base raised $60,000 via internet to fund US tour.

- In 2001, 12,000 fans “pre-ordered” new album 12 months in advance resulted in “Anoraknophobia”.

• 2000: Brian Camelio founded ArtistShare:

- Considered internet’s first crowdfunding website.

- Fans finance production costs and get favourable terms.

- Patent US7885887B2 filed in 2003.

Crowdfunding started to get big from 2009 onwards

2009: Crowdfunding gets big:

• Crowdfunding platforms emerge:

- Indiegogo 2008 -> “reward-based crowdfunding”.

- Kickstarter 2009 -> “reward-based crowdfunding”.

- GoFundMe 2010 -> “donation-based crowdfunding”.

• 2011: Patent law suit: Kickstarter vs. ArtistShare.

- ArtistShare: “Kickstarter infringes our patent”.

- Kickstarter: “Practice of crowdfunding not invented by ArtistShare. Fundamental economic practice.”

- June 2015: Judge rules in favour of Kickstarter.

인터넷 크라우드펀딩의 시작 (1997년)

인터넷 크라우드펀딩은 1997년에 처음 시작되었습니다. 다음은 초기 사례들입니다:

- 1997년: 영국 록 밴드 마릴리언 (Marillion)

- 미국 팬들이 인터넷을 통해 60,000달러를 모아 마릴리언의 미국 투어 자금을 마련했습니다.

- 2001년에는 12,000명의 팬들이 새 앨범을 12개월 앞서 "선주문"하여, 그 결과로 앨범 "Anoraknophobia"가 발매되었습니다.

- 2000년: 브라이언 카멜리오 (Brian Camelio)가 ArtistShare 설립

- ArtistShare는 인터넷 최초의 크라우드펀딩 웹사이트로 여겨집니다.

- 팬들이 아티스트의 제작 비용을 지원하고, 그 대가로 유리한 조건을 제공받았습니다.

- 2003년에 특허 US7885887B2를 출원했습니다.

크라우드펀딩의 대중화 (2009년부터)

2009년부터 크라우드펀딩은 본격적으로 대중화되기 시작했습니다. 주요 발전 사항은 다음과 같습니다:

- 크라우드펀딩 플랫폼의 등장

- Indiegogo (2008년 설립): 보상 기반 크라우드펀딩 플랫폼.

- Kickstarter (2009년 설립): 보상 기반 크라우드펀딩 플랫폼.

- GoFundMe (2010년 설립): 기부 기반 크라우드펀딩 플랫폼.

- 2011년: 특허 소송 - Kickstarter vs. ArtistShare

- ArtistShare: "Kickstarter가 우리의 특허를 침해했다"고 주장.

- Kickstarter: "크라우드펀딩의 실행은 ArtistShare가 발명한 것이 아니며, 이는 기본적인 경제적 관행이다"라고 반박.

- 2015년 6월: 판사는 Kickstarter의 손을 들어주었습니다. 이는 크라우드펀딩이 일반적인 경제적 관행으로 인정받았음을 의미합니다.

이와 같이 크라우드펀딩은 인터넷을 통해 시작되어 점차 대중화되었으며, 다양한 플랫폼이 등장하면서 더욱 활성화되었습니다.

Statue of Liberty pedestal crowdfunded in 1885

Crowdfunding much older than that

“Let us not wait for the millionaires to give us this money. It is not a gift from the millionaires of France to the millionaires of America, but a gift of the whole people of France to the whole people of America.”

Joseph Pulitzer

Publisher of New York World

16 March 1885

- 160k people raised $101,091 (100k required), 90% gave less than $1.

자유의 여신상 받침대를 세우기 위해 1885년에 진행된 크라우드펀딩은, 현대의 인터넷 크라우드펀딩보다 훨씬 오래된 개념입니다. 당시 뉴욕 월드의 발행인 조셉 퓰리처는 대중에게 자금 모금에 참여할 것을 호소했으며, 160,000명의 사람들이 모금에 참여하여 총 $101,091를 모았습니다. 이 중 90%는 $1 이하의 소액 기부였으며, 목표 금액은 $100,000이었습니다. 퓰리처는 이 모금이 프랑스의 백만장자들이 아닌 프랑스 전체 국민이 미국 전체 국민에게 주는 선물이라고 강조했습니다.

3. What is Crowdfunding?

Crowdfunding enables people to pool small amounts

Definition Crowdfunding:

“Form of capital raising whereby groups of people pool money, typically comprised of very small individual

contributions, to support an effort by others to accomplish a specific goal.”

Testimony on Crowdfunding and Capital Formation

Online, peer‐to‐peer, crowd‐led marketplaces that are open at least partially to individual retail investors (the

“crowd”).

Rau (2019)

크라우드펀딩이란 많은 사람들이 소액의 자금을 모아 특정 프로젝트나 아이디어, 비즈니스를 지원하는 방식입니다.

크라우드펀딩의 주요 특징과 유형을 다음과 같이 설명할 수 있습니다:

크라우드펀딩의 주요 특징

- 다수의 기여자: 수많은 사람들이 소액을 기부하거나 투자합니다.

- 인터넷 기반: 주로 인터넷 플랫폼을 통해 진행됩니다.

- 목표 금액: 프로젝트나 아이디어를 실현하기 위해 특정 금액을 목표로 설정합니다.

- 보상 구조: 기여자들은 프로젝트의 성공 여부에 따라 보상(제품, 서비스, 수익 배분 등)을 받을 수 있습니다.

크라우드펀딩의 유형

- 보상 기반 크라우드펀딩:

- 기여자들이 금액에 따라 다양한 형태의 보상을 받습니다.

- 예: Kickstarter, Indiegogo

- 보상 예시: 제품의 초기 버전, 한정판 아이템 등

- 기부 기반 크라우드펀딩:

- 기여자들이 기부를 통해 프로젝트를 지원하며, 금전적인 보상은 받지 않습니다.

- 예: GoFundMe

- 주로 자선 활동, 의료비 지원, 비영리 프로젝트 등에 사용됩니다.

- 투자 기반 크라우드펀딩:

- 기여자들이 금전적인 이익을 기대하며 투자합니다.

- 주식, 채권, 지분 참여 등의 형태로 보상을 받습니다.

- 예: Seedrs, Crowdcube

- 대출 기반 크라우드펀딩:

- 기여자들이 프로젝트나 사업에 대출을 해주고, 이자를 받습니다.

- 예: LendingClub, Funding Circle

크라우드펀딩은 스타트업, 창작자, 자선단체 등 다양한 분야에서 자금을 조달하는 유용한 방법으로 자리잡고 있습니다. 이를 통해 기존의 금융 기관을 거치지 않고도 많은 사람들에게 아이디어를 알리고, 필요한 자금을 빠르게 모을 수 있습니다.

Crowdfunding as form of financial intermediation

| Investors |

Platforms | Entrepreneurs |

| Crowdfunders (all types) • Access to entrepreneurs • Community participation • Access to products • Low-cost format contract • Returns (equity, debt) |

Platform intermediaries • Standardized contract at standardized fee • Mitigate information problems • Match investors and entrepreneurs • Due diligence, certification |

• Access to investors • Low cost of raising capital relative to alternatives • Advice from platforms • Information about the demand for their product (traction) • Loss of secrecy (cost of competition/replication) • Publicity |

A general typology of crowdfunding models

Examples:

Donation-based: GoFundMe, Wonderful.org

Reward-based: Indiegogo, Kickstarter

Equity-based: Crowdcube (52% market share in UK), Seedrs

Debt-based: FundingCircle (72% SME lending), LendInvest

Crowdfunding models differ in complexity

Uncertainty/complexity in different types of crowdfunding

4. Types of crowdfunding models

4.1 Reward-based

Typically, pre-purchase and rewards are combined

Reward funding models

• Pre-purchase:

Receive product or right to buy at reduced price.

• Rewards (conditional on $-backing)

“Thank you” card, name listed on website, T-shirt, invitation to event, combo packs, work with creator, etc.

- Typically combines reward and pre-purchase model.

Griffin (2012) and https://www.dummies.com/article/business-careers-money/business/strategicplanning/use-reward-based-crowdfunding-business-plan-223439/

보상 기반 크라우드펀딩 (Reward-based Crowdfunding)

보상 기반 크라우드펀딩은 프로젝트에 자금을 지원하는 사람들에게 다양한 형태의 보상을 제공하는 방식입니다.

이 방식은 주로 사전 구매(pre-purchase)와 보상(rewards)을 결합하여 사용됩니다.

보상 펀딩 모델

- 사전 구매 (Pre-purchase)

- 자금을 지원한 사람은 제품을 받거나 할인된 가격에 구매할 권리를 얻습니다.

- 보상 (Rewards)

- 자금 지원 금액에 따라 다양한 보상을 받습니다. 보상 예시로는 감사 카드, 웹사이트에 이름 기재, 티셔츠, 이벤트 초대, 콤보 팩, 창작자와의 협업 등이 있습니다.

- 이러한 보상은 특정 금액 이상을 지원해야 받을 수 있습니다.

보통 보상 기반 크라우드펀딩은 사전 구매와 보상 모델을 결합하여 진행됩니다.

dummies - Learning Made Easy

For the Exam-Season Crammer Calling all bookworms and teacher’s pets! The moment you’ve been stressing for so long is nigh. Get ready for exam season by learning how best to study for your tests, what foods to feed your overworked brain, and what to do

www.dummies.com

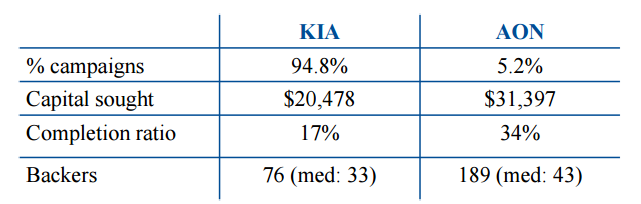

Two reward models exist but KIA most common

Reward funding models

All-or-nothing (AON) <--> Keep-it-all (KIA)

• Indiegogo allows choices between AON and KIA.

- Entrepreneurs reduce their own risk by opting for KIA at expense of achieving higher funding.

두 가지 보상 모델

크라우드펀딩에는 두 가지 보상 모델이 있으며, 대부분의 플랫폼은 두 모델 중 하나를 선택할 수 있게 합니다:

- All-or-nothing (AON)

- 목표 금액을 모두 달성해야 자금을 받을 수 있습니다.

- 목표 금액을 달성하지 못하면 자금을 받지 못합니다.

- Keep-it-all (KIA)

- 목표 금액을 달성하지 못하더라도 모인 자금을 모두 유지할 수 있습니다.

- 목표 금액을 달성하지 않아도 자금을 사용할 수 있습니다.

Indiegogo의 선택 옵션

- Indiegogo 플랫폼은 창작자들이 AON과 KIA 중에서 선택할 수 있도록 합니다.

- 창작자들이 KIA 모델을 선택하면 목표 금액을 달성하지 못하더라도 모인 자금을 유지할 수 있어 자신들의 리스크를 줄일 수 있습니다. 하지만 이는 더 높은 자금을 모을 수 있는 가능성을 줄일 수 있습니다.

요약

보상 기반 크라우드펀딩은 사전 구매와 보상을 결합하여 자금을 모으는 방식으로, 자금 지원자들에게 다양한 형태의 보상을 제공합니다. 두 가지 주요 보상 모델(AON, KIA)이 있으며, 플랫폼에 따라 창작자들이 원하는 모델을 선택할 수 있습니다. KIA 모델은 리스크를 줄일 수 있지만, 더 높은 자금을 모으는 데는 불리할 수 있습니다.

Compared to traditional finance, no dilution for the founder

Advantages for entrepreneur

1. No dilution:

- Equity financing requires giving up ownership.

2. No financial obligation or penalty.

- Debt requires interest, and repayment; may include collateral or covenants.

- 84% of Kickstarter’s top projects shipped late.*

3. Standardized contractual terms.

4. Feedback from investors/future customers.

전통적인 금융과 비교하여 창업자에게 유리한 점

- 지분 희석 없음 (No dilution)

- 전통적인 주식 자금 조달은 창업자가 회사의 소유권 일부를 포기해야 하지만, 크라우드펀딩은 그렇지 않습니다.

- 금융 의무나 페널티 없음

- 대출은 이자와 상환 의무가 있으며, 담보나 계약 조건이 포함될 수 있습니다.

- 그러나 크라우드펀딩은 이러한 금융 의무나 페널티가 없습니다.

- Kickstarter의 상위 84% 프로젝트가 기한을 넘기긴 했지만, 이는 금융 의무가 아닌 프로젝트 지연에 해당됩니다.

- 표준화된 계약 조건

- 크라우드펀딩은 대개 표준화된 계약 조건을 가지고 있어 창업자가 복잡한 금융 계약에 신경 쓸 필요가 없습니다.

- 투자자 및 미래 고객으로부터의 피드백

- 크라우드펀딩을 통해 창업자는 초기 투자자나 미래 고객으로부터 직접적인 피드백을 받을 수 있습니다.

Greater transparency may mean theft and is costly

Disadvantages for entrepreneur

1. Plagiarism / Theft.

2. Early publicity and failure could make future crowdfunding harder.

3. Reporting and communication costs could be high.

크라우드펀딩의 단점

- 표절 / 도난

- 아이디어가 공공에 노출됨으로써 다른 사람들이 아이디어를 훔치거나 표절할 위험이 있습니다.

- 초기 홍보와 실패

- 크라우드펀딩 초기의 과도한 홍보와 실패는 향후 크라우드펀딩을 더 어렵게 만들 수 있습니다.

- 보고 및 소통 비용

- 자금 지원자들과의 보고 및 소통에 드는 비용이 높을 수 있습니다.

요약

크라우드펀딩은 창업자가 회사의 소유권을 포기하지 않고 자금을 모을 수 있는 방법으로, 금융 의무나 복잡한 계약 조건 없이 초기 투자자나 고객으로부터 피드백을 받을 수 있는 장점이 있습니다. 그러나 아이디어 도난, 초기 홍보와 실패의 위험, 그리고 보고 및 소통 비용이 단점으로 작용할 수 있습니다.

How Kickstarter helped blockchain innovation

Example: Funding blockchain project

• First blockchain projects funded by Kickstarter

• Chris Cassano, founder of Piper: paper wallet.

- Wallet = app that is similar to bank account.

- Keeping private key online, makes you subject to hacks.

- Paper wallet: print out code and store it off-line.

Created prototype-dedicated printer based on Raspberry Pi.

- Posted description on Kickstarter:

- Sold 25, netted him $4,000.

Kickstarter가 블록체인 혁신을 도운 방법

블록체인 프로젝트의 자금 조달

Kickstarter는 초기 블록체인 프로젝트의 자금 조달에 큰 도움을 주었습니다.

첫 블록체인 프로젝트들 중 하나는 크리스 카사노(Chris Cassano)가 창립한 Piper였습니다.

Chris Cassano와 Piper 프로젝트

- 지갑(Wallet): 지갑은 은행 계좌와 유사한 앱으로, 사용자의 암호화폐를 저장하는 역할을 합니다.

- 온라인 개인 키 보관의 문제점: 온라인에 개인 키를 보관하면 해킹의 위험이 있습니다.

- 종이 지갑(Paper Wallet): Piper 프로젝트는 개인 키를 오프라인으로 안전하게 보관할 수 있는 종이 지갑을 만들었습니다. 종이 지갑은 코드를 인쇄하여 오프라인에 저장하는 방식입니다.

- 프로토타입 전용 프린터: Piper는 Raspberry Pi를 기반으로 한 프로토타입 전용 프린터를 제작하여 종이 지갑을 쉽게 인쇄할 수 있도록 했습니다.

Kickstarter 캠페인

- Kickstarter에 프로젝트 게시: Chris Cassano는 자신의 프로젝트를 Kickstarter에 게시했습니다.

- 판매 및 수익: 프로젝트를 통해 25개의 프린터를 판매하여 $4,000의 수익을 올렸습니다.

요약

Kickstarter는 블록체인 혁신을 지원하는 중요한 플랫폼 역할을 했습니다. Chris Cassano의 Piper 프로젝트는 Kickstarter를 통해 종이 지갑을 위한 전용 프린터를 제작하고 판매하여 초기 자금을 조달할 수 있었습니다. 이를 통해 블록체인 프로젝트들이 자금을 모으고, 아이디어를 실현할 수 있는 기회를 제공했습니다.

Campaigns can be for simple and complex products

Range of crowdfunding campaigns

As reward crowd-funder, no cash flow rights

The controversy: Oculus Rift

• Kickstarter campaign on 1 August 2012. Target: $250k.

- Within 24hrs, reached $2.5mio (10,000 backers).

• March 2013: Dev kits ship to backers.

• June + Dec 2013: $16m + $75m investor funding.

• March 2014: 60,000 dev kits sold.

• 25 March 2014: Facebook acquires Oculus Rift for $2billion -> so far, no retail products shipped.

• Jan 2016: Original backers will get free Rift.

보상 기반 크라우드펀딩의 특징: 현금 흐름 권리가 없음

사례: 오큘러스 리프트(Oculus Rift)의 논란

오큘러스 리프트는 보상 기반 크라우드펀딩의 대표적인 사례로, 다음과 같은 과정으로 진행되었습니다.

- Kickstarter 캠페인 (2012년 8월 1일)

- 목표 금액: $250,000

- 24시간 내에 $2,500,000를 모금하였고, 약 10,000명의 후원자를 모았습니다.

- 2013년 3월

- 개발자 키트(Dev kits)를 후원자들에게 배송 시작.

- 2013년 6월과 12월

- 투자자들로부터 각각 $16백만과 $75백만의 추가 자금 조달.

- 2014년 3월

- 총 60,000개의 개발자 키트가 판매됨.

- 2014년 3월 25일

- 페이스북이 오큘러스 리프트를 $2억 달러에 인수. 이 시점까지는 소매용 제품이 출하되지 않았음.

- 2016년 1월

- 초기 후원자들에게 무료로 Rift를 제공하겠다고 발표.

논란의 요지

오큘러스 리프트의 Kickstarter 캠페인은 성공적이었으나, 몇 가지 논란이 발생했습니다:

- 현금 흐름 권리 없음: 보상 기반 크라우드펀딩의 후원자들은 현금 흐름에 대한 권리가 없습니다. 즉, 후원자들은 투자자와 달리 회사의 수익에 대한 지분이나 배당금을 받지 못합니다.

- 대규모 인수: 페이스북이 오큘러스를 거액에 인수하면서 초기 후원자들은 자신들이 받는 보상이 상대적으로 적다는 불만을 가졌습니다.

- 제품 배송 지연: 페이스북 인수 당시까지 소매용 제품이 출하되지 않았고, 초기 후원자들은 자신들이 지원한 프로젝트의 성과를 직접적으로 체험하지 못했습니다.

요약

오큘러스 리프트의 사례는 보상 기반 크라우드펀딩의 장단점을 잘 보여줍니다. 후원자들은 프로젝트를 실현시키기 위해 자금을 제공하지만, 그 대가로 현금 흐름에 대한 권리는 받지 못합니다. 이로 인해, 후속 투자와 인수 과정에서 상대적으로 불리한 위치에 놓일 수 있습니다. 그러나 오큘러스 리프트의 경우처럼, 때로는 추가적인 보상(예: 무료 제품)이 제공되기도 합니다.

Typical timeline of project on Kickstarter

4.2 Equity-based

Equity crowdfunding platforms offer different models

Different platform models

• Investment type:

- Direct model (e.g. Crowdcube).

Nominee model (e.g. Seedrs).

- Coinvestment model (e.g. SyndicateRoom).

• Mainly AON (a few KIA) or choice btw. the two.

• Voting vs. non-voting shares.

지분 기반 크라우드펀딩 (Equity-based Crowdfunding)

지분 기반 크라우드펀딩은 투자자들이 기업의 지분을 얻는 방식으로, 여러 모델이 존재합니다. 이를 통해 투자자들은 회사의 일부 소유권을 가지게 되며, 회사의 성장과 함께 이익을 나눌 수 있습니다.

다양한 플랫폼 모델

지분 기반 크라우드펀딩 플랫폼은 각기 다른 모델을 제공합니다:

- 투자 유형

- 직접 모델 (Direct model): 투자자들이 직접 회사의 주식을 소유합니다.

- 예: Crowdcube

- 명목 모델 (Nominee model): 플랫폼이 투자자들을 대신하여 주식을 소유합니다.

- 예: Seedrs

- 공동 투자 모델 (Coinvestment model): 플랫폼이 다른 주요 투자자들과 함께 투자를 진행합니다.

- 예: SyndicateRoom

- 직접 모델 (Direct model): 투자자들이 직접 회사의 주식을 소유합니다.

- 펀딩 모델

- 대부분의 지분 기반 크라우드펀딩은 All-or-Nothing (AON) 모델을 사용합니다. 이는 목표 금액을 모두 달성해야 자금을 받을 수 있는 방식입니다.

- 일부 플랫폼은 Keep-it-All (KIA) 모델을 제공하기도 하며, 목표 금액을 달성하지 못하더라도 모금된 금액을 유지할 수 있습니다.

- 몇몇 플랫폼은 AON과 KIA 중 선택할 수 있게 합니다.

- 투표권 여부

- 투표권 주식 (Voting shares): 투자자들이 회사의 중요한 결정에 투표할 수 있는 권리를 가집니다.

- 비투표권 주식 (Non-voting shares): 투자자들이 회사의 결정에 투표할 수 있는 권리가 없습니다.

요약

지분 기반 크라우드펀딩은 투자자들이 회사의 지분을 얻어 이익을 공유하는 방식입니다. 플랫폼은 직접 모델, 명목 모델, 공동 투자 모델 등의 다양한 모델을 제공하며, 펀딩 방식으로는 대부분 AON을 사용하지만 일부는 KIA도 선택할 수 있습니다. 또한, 투자자들이 투표권을 가지는지 여부에 따라 투표권 주식과 비투표권 주식으로 나뉩니다.

Seedrs and others in UK regulated by FCA

Example Seedrs

• Founded as part of MBA project at Said Business School; launched on 6 July 2012.

• Vets each campaign for fair/accurate statements.

• First equity crowdfunding platform to receive regulatory approval from a financial regulator.

Seedrs와 영국의 규제

Seedrs는 영국에서 금융감독청(FCA)의 규제를 받는 지분 기반 크라우드펀딩 플랫폼입니다.

Seedrs의 예

- 설립 배경: 옥스퍼드 대학의 사이드 비즈니스 스쿨(Said Business School)에서 MBA 프로젝트의 일환으로 설립되었습니다. 2012년 7월 6일에 런칭했습니다.

- 캠페인 검토: 각 캠페인을 공정하고 정확한 내용인지 검토합니다.

- 규제 승인: 금융 규제 기관으로부터 규제 승인을 받은 최초의 지분 기반 크라우드펀딩 플랫폼입니다.

Unanswered governance issues in equity crowdfunding

Governance issues

• Adverse selection: are ventures high or low quality?

• Quality of platform screening (due diligence)?

- Platform moral hazard: fixed vs. variable fee, firms/employee ratio.

• Who is monitoring entrepreneurs post-funding?

- Free riding: Direct vs. nominee vs. co-investment model.

• Entrepreneur signalling: board of directors, ownership structure, share vesting upon milestone achievement.

지분 기반 크라우드펀딩의 미해결된 거버넌스 문제

지분 기반 크라우드펀딩에는 몇 가지 중요한 거버넌스 문제가 있습니다:

- 역선택 (Adverse selection)

- 투자할 벤처가 고품질인지 저품질인지에 대한 문제입니다.

- 플랫폼 스크리닝의 품질 (Quality of platform screening)

- 플랫폼의 실사(due diligence) 품질은 얼마나 신뢰할 수 있는가?

- 플랫폼의 도덕적 해이 (moral hazard): 고정 수수료와 변동 수수료, 그리고 기업/직원 비율에 따른 문제가 있습니다.

- 자금 조달 후 기업가 모니터링 (Monitoring entrepreneurs post-funding)

- 무임승차 문제 (Free riding): 자금 조달 후 누가 기업가를 모니터링하는가? 직접 모델, 명목 모델, 공동 투자 모델 중 어느 것이 적합한가?

- 기업가의 신호 발송 (Entrepreneur signalling)

- 이사회 구성, 소유 구조, 목표 달성 시 주식 베스팅(share vesting) 등을 통해 기업가가 어떻게 신뢰를 형성하는가?

요약

Seedrs는 영국에서 규제를 받는 지분 기반 크라우드펀딩 플랫폼으로, 각 캠페인의 공정성과 정확성을 검토합니다. 지분 기반 크라우드펀딩에는 역선택, 플랫폼 스크리닝의 품질, 자금 조달 후 모니터링, 기업가의 신호 발송 등 여러 거버넌스 문제가 있습니다. 이러한 문제들은 플랫폼의 신뢰성과 투자자 보호를 위해 해결되어야 합니다.

Equity-based crowdfunding requires special law

Equity crowdfunding legislation

• Equity crowdfunding model violated US securities law.

- Securities Act 1933

- 5 April 2012: Jumpstart Our Business Startups (JOBS) Act.

• In UK: Financial Services and Markets Act.

- Must be regulated by FCA and adhere to regulations.

Additional tax incentive schemes in UK:

• UK: 6 April 2012: Seed Enterprise Investment Scheme (SEIS).

지분 기반 크라우드펀딩과 관련 법규

미국의 지분 기반 크라우드펀딩 법규

지분 기반 크라우드펀딩은 일반적으로 증권법의 적용을 받으며, 미국에서는 다음과 같은 법규로 규제됩니다:

- 증권법 1933 (Securities Act 1933)

- 이 법에 따르면, 증권을 발행하거나 판매하려면 특정 규정을 준수해야 합니다.

- 지분 기반 크라우드펀딩은 이 법을 위반할 가능성이 있었습니다.

- JOBS Act (2012년 4월 5일)

- "Jumpstart Our Business Startups" 법으로, 지분 기반 크라우드펀딩을 합법화하고 규제하기 위해 제정되었습니다.

- 이 법은 스타트업과 소규모 기업이 더 쉽게 자금을 조달할 수 있도록 도와줍니다.

영국의 지분 기반 크라우드펀딩 법규

영국에서도 지분 기반 크라우드펀딩은 규제를 받습니다:

- 금융 서비스 및 시장법 (Financial Services and Markets Act)

- 지분 기반 크라우드펀딩 플랫폼은 금융감독청(FCA)의 규제를 받아야 하며, 해당 규정을 준수해야 합니다.

- 추가 세금 인센티브 제도

- Seed Enterprise Investment Scheme (SEIS) (2012년 4월 6일 도입)

- 이 제도는 스타트업에 투자하는 개인 투자자에게 세금 혜택을 제공합니다.

- SEIS는 스타트업과 소규모 기업에 대한 투자를 촉진하기 위해 설계되었습니다.

- Seed Enterprise Investment Scheme (SEIS) (2012년 4월 6일 도입)

요약

지분 기반 크라우드펀딩은 증권법의 적용을 받기 때문에 특별한 법규가 필요합니다. 미국에서는 증권법 1933을 준수하기 위해 JOBS Act가 제정되었고, 영국에서는 금융 서비스 및 시장법에 따라 FCA의 규제를 받아야 합니다. 또한, 영국은 SEIS와 같은 세금 인센티브 제도를 통해 스타트업에 대한 투자를 장려하고 있습니다.

4.3 Debt-based

Two types of debt-based crowdfunding exist

Marketplace lending and P2P lending

• Marketplace lending or peer-to-peer (P2P) lending.

- Sectors: business loans, consumer loans, invoice-backed loans, and property-backed loans.

• Contributors lend entrepreneur (consumer) money.

- Repayment at end of period.

- Some contributors also receive interest.

- E.g. no interest on Kiva.org.

• Not substitute to banks but rather complement.

채권 기반 크라우드펀딩 (Debt-based Crowdfunding)

채권 기반 크라우드펀딩의 두 가지 유형

- 마켓플레이스 대출 (Marketplace lending)

- P2P 대출 (Peer-to-peer lending)

주요 특징

- 마켓플레이스 대출과 P2P 대출

- 이 두 가지 유형은 비슷하지만,

주로 비즈니스 대출, 소비자 대출, 청구서 담보 대출, 부동산 담보 대출 등의 분야에서 사용됩니다.

- 이 두 가지 유형은 비슷하지만,

- 자금 제공자

- 자금 제공자들은 기업가(또는 소비자)에게 돈을 빌려줍니다.

- 일정 기간이 끝난 후 원금을 상환받습니다.

- 일부 자금 제공자들은 이자도 받습니다.

- 예를 들어, Kiva.org에서는 이자가 없는 대출도 있습니다.

- 은행의 대체재가 아닌 보완재

- 채권 기반 크라우드펀딩은 은행을 대체하는 것이 아니라, 은행 대출을 보완하는 역할을 합니다.

요약

채권 기반 크라우드펀딩은 마켓플레이스 대출과 P2P 대출 두 가지 유형이 있으며, 이는 비즈니스 대출, 소비자 대출, 청구서 담보 대출, 부동산 담보 대출 등 다양한 분야에서 사용됩니다. 자금 제공자들은 기업가나 소비자에게 돈을 빌려주고, 일정 기간 후 원금을 상환받으며, 일부는 이자를 받기도 합니다. 이 방식은 은행 대출을 대체하는 것이 아니라, 보완하는 역할을 합니다.

Debt-based crowdfunding consists of 4 broad sectors

Funding circle projects expected returns btw. 4.5-6.5%

Marketplace lending– Example FundingCircle:

• Founded August 2010: business loans.

• Credit assessment team checks creditworthiness.

• Lending option: Balanced (4.5-6.5%), Conservative (4.3-4.7%).

• 1% annual servicing fee.

• Average business: 9 years old, 6 employees, £800,000 turnover.

Closed lending option to retail investors in by March 2022. Started to provide Coronarelief business interruption loans – retail investors not permitted.

Investment through Funding circle invovles leading to small nad medium sized businesses, so your investment can go down as well as up. Funding Circle Limited is authorised and regulated by the Financial Circle is not covered byt he Financial Services Compensation sheme. Registered in England (Co. No. 0696588) with registered office at 71 Queen Victoria Street, london.

FundingCircle은 중소기업에 대출을 제공하는 채권 기반 크라우드펀딩 플랫폼으로, 투자자들은 균형형과 보수형 대출 옵션을 선택할 수 있으며, 각각 예상 수익률은 4.5-6.5%와 4.3-4.7%입니다. 신용 평가 팀이 대출자의 신용도를 검토하며, 연간 1%의 서비스 수수료가 부과됩니다. 2022년 3월 이후로 소매 투자자에게 대출 옵션을 제공하지 않으며, 코로나 구제 비즈니스 대출을 제공합니다. 투자에는 리스크가 있으며, 금융 서비스 보상 제도에 포함되지 않습니다.

Zopa projects expected returns btw. 3.9-4.6%

P2P lending– Example Zopa:

• Founded March 2005: 1st P2P lending company.

• Borrowers can take out loans btw. £1,000 and £25,000.

- For: cars, tools, homes, debt consolidation, others…

• Screens borrowers, approves 20%, assigns risk scores.

- Diversifies your investment across borrowers and provides two investment options (Zopa Core or Plus).

• Was granted banking licence in 2019 (“Zopa bank”).

- Zopa exited P2P lending business in December 2021. Now, focus on banking products

(saving accounts, credit cards auto/house/tool loans).

Zopa limited is authorised and regulated by the Financial Conduct Authority, and entered on the Financial Services Register. Zopa Bank limited is authorised byt he Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority.

Zopa는 세계 최초의 P2P 대출 플랫폼으로, 개인 간 대출을 중개합니다. 대출 금액은 £1,000에서 £25,000 사이이며, 대출 신청자의 20%만 승인됩니다. 투자자들은 Zopa Core와 Zopa Plus 옵션을 통해 투자할 수 있으며, 각각의 예상 수익률은 3.9-4.6%입니다. 2019년에 은행 인가를 받아 "Zopa Bank"로 전환되었으며, 2021년에는 P2P 대출 사업을 종료하고 은행 상품에 집중하고 있습니다. Zopa는 금융감독청(FCA)과 프루덴셜 규제 당국의 규제를 받습니다.

Simple Crowdfunding focuses on real estate

P2P lending– Example Simple Crowdfunding:

• Founded 2013. Focus on property investments.

• Minimum investment: 100GBP.

• Works with property developers to supply property opportunities.

• Funding on both an equity and debt basis.

Simple crowdfunding is a trading name for both Focus 2020 Limited and SImple Property Ltd. Focus 2020 Limited is authorised and regulated by the Financial Conduct Authority. Siomple Property Ltd is an appinited representative of share in ltd, authorised and regulated by the Finanical Conduct Authority. Focus 2020 Limited and simple property ltd are registeed companies in Enlgand and Wales.

Simple Crowdfunding은 부동산 투자에 특화된 P2P 대출 플랫폼으로, 2013년에 설립되었습니다. 최소 투자 금액은 £100이며, 부동산 개발자와 협력하여 다양한 부동산 투자 기회를 제공합니다. 지분 및 채권 기반으로 자금을 조달하며, 두 회사인 Focus 2020 Limited와 Simple Property Ltd가 운영합니다. 두 회사 모두 금융감독청(FCA)의 규제를 받습니다.

5. Who benefits from crowdfunding?

Providing small firms financing can enhance innovation

Access to Finance – Gov’t R&D subsidies

• Gov’t subsidies to small firms could be good or bad

- US Department of Energy Small Business Innovation

Research program, Phase 1 awards:

• Double probability of firm receiving VC funding.

• Double probability of positive revenue.

• Increases probability of survival and successful exit.

• More useful for hardware firms which require greater upfront capital (more financially constraint).

Access to investments must also protect investors

Screening and fraud prediction

• With subsidies, gov’t is doing screening.

• Quality of screening on crowdfunding platforms?

- Kickstarter stricter than Indiegogo.

- Who is doing post-equity funding governance?

• Evidence suggests that crowdfunding fraud related to:

- Entrepreneurs’ characteristics.

- Social media affinity.

- Campaign funding and reward structure.

- Campaign description.

누가 크라우드펀딩의 혜택을 받는가?

크라우드펀딩은 특히 소규모 기업들에게 자금을 제공함으로써 혁신을 촉진할 수 있습니다.

자금 접근성 - 정부의 연구 개발(R&D) 보조금

- 정부 보조금의 영향

- 소규모 기업에게 정부 보조금이 긍정적일 수도 있고 부정적일 수도 있습니다.

- 미국 에너지부의 소규모 비즈니스 혁신 연구 프로그램 (SBIR)

- 1단계 보조금의 효과:

- 기업이 벤처 캐피탈(VC) 자금을 받을 확률을 두 배로 증가시킵니다.

- 긍정적인 수익을 올릴 확률을 두 배로 증가시킵니다.

- 생존과 성공적인 종료(Exit) 가능성을 높입니다.

- 특히 더 많은 초기 자본이 필요한 하드웨어 기업에게 유용합니다.

- 1단계 보조금의 효과:

투자 접근성과 투자자 보호

- 스크리닝 및 사기 예측

- 정부 보조금의 경우, 정부가 스크리닝을 수행합니다.

- 크라우드펀딩 플랫폼의 스크리닝 품질은 어떻게 되는가?

- Kickstarter가 Indiegogo보다 더 엄격한 스크리닝 절차를 가집니다.

- 누가 자금 조달 후 거버넌스를 수행하는가?

- 크라우드펀딩 사기 관련 증거

- 기업가의 특성

- 소셜 미디어 친화도

- 캠페인 자금 조달 및 보상 구조

- 캠페인 설명

요약

크라우드펀딩은 소규모 기업들에게 자금을 제공하여 혁신을 촉진할 수 있습니다. 정부의 연구 개발 보조금은 기업의 생존과 성공을 도울 수 있지만, 크라우드펀딩 플랫폼의 스크리닝 품질이 중요합니다. Kickstarter가 Indiegogo보다 더 엄격한 스크리닝 절차를 가지고 있으며, 사기 예측에는 기업가의 특성, 소셜 미디어 친화도, 캠페인 구조와 설명 등이 관련됩니다.

Readings for this lecture

1) Berk and DeMarzo, “Corporate Finance”, Chapter 23.

2) Links provided on the slides.

3) Cumming and Johan, “Crowdfunding

After the lecture, you will understand:

• Describe the traditional ways of how equity capital is being raised.

Traditional Ways of Raising Equity Capital

- Venture Capital (VC)

- VC firms provide funding to startups and small businesses with long-term growth potential. In exchange, they take an equity stake in the company.

- VCs often offer not just funding, but also mentorship, industry connections, and strategic advice.

- Angel Investors

- Wealthy individuals who invest their personal funds into early-stage companies.

- They typically take a hands-on approach, offering advice and industry expertise in addition to capital.

- Initial Public Offering (IPO)

- Companies sell shares to the public for the first time on a stock exchange.

- This method is used by more mature companies seeking to raise large amounts of capital and expand their market presence.

- Private Equity

- Investment firms invest in companies that are not publicly traded, often taking a significant or controlling stake.

- Private equity firms focus on restructuring and improving companies to increase their value before eventually exiting through a sale or IPO.

- Family and Friends

- Early-stage businesses often raise capital from personal connections.

- This method is informal and relies on the trust and personal relationships between the business owner and investors.

전통적인 지분 자금 조달 방법

- 벤처 캐피탈 (Venture Capital, VC)

- VC 회사는 장기 성장 가능성이 있는 스타트업 및 중소기업에 자금을 제공합니다. 그 대가로 회사의 지분을 받습니다.

- VC는 자금뿐만 아니라 멘토링, 산업 연결 및 전략적 조언도 제공합니다.

- 엔젤 투자자 (Angel Investors)

- 개인 자금을 초기 단계의 기업에 투자하는 부유한 개인들입니다.

- 이들은 자금 외에도 조언과 산업 전문 지식을 제공합니다.

- 기업공개 (Initial Public Offering, IPO)

- 기업이 처음으로 주식을 공개적으로 판매하여 자금을 조달합니다.

- 이 방법은 성숙한 기업이 대규모 자금을 모으고 시장 존재감을 확장하는 데 사용됩니다.

- 프라이빗 에쿼티 (Private Equity)

- 투자 회사가 비상장 기업에 투자하여 상당한 지분을 취득합니다.

- 프라이빗 에쿼티 회사는 기업의 구조 조정 및 개선을 통해 가치를 높이고, 이후 매각 또는 IPO를 통해 출구를 모색합니다.

- 가족과 친구 (Family and Friends)

- 초기 단계의 기업이 개인적인 인맥을 통해 자금을 조달합니다.

- 이 방법은 비공식적이며, 사업주와 투자자 간의 신뢰와 개인적인 관계에 의존합니다.

• Define crowdfunding and its different types.

Crowdfunding and Its Different Types

Crowdfunding is a method of raising funds from a large number of people, typically via the internet. Different types of crowdfunding include:

- Reward-based Crowdfunding

- Backers receive rewards or products in return for their contributions.

- Examples: Kickstarter, Indiegogo

- Equity-based Crowdfunding

- Investors receive shares of the company in exchange for their investment.

- Examples: Seedrs, Crowdcube

- Debt-based Crowdfunding (P2P Lending)

- Investors lend money to individuals or businesses and receive interest payments.

- Examples: FundingCircle, Zopa

- Donation-based Crowdfunding

- Donors contribute to a cause or project without expecting any financial return.

- Examples: GoFundMe, JustGiving

크라우드펀딩 정의 및 종류

크라우드펀딩은 인터넷을 통해 많은 사람들로부터 자금을 모으는 방법입니다. 크라우드펀딩의 종류는 다음과 같습니다:

- 보상 기반 크라우드펀딩 (Reward-based Crowdfunding)

- 후원자는 기여에 대한 보상이나 제품을 받습니다.

- 예: Kickstarter, Indiegogo

- 지분 기반 크라우드펀딩 (Equity-based Crowdfunding)

- 투자자는 투자 대가로 회사의 주식을 받습니다.

- 예: Seedrs, Crowdcube

- 채권 기반 크라우드펀딩 (Debt-based Crowdfunding, P2P Lending)

- 투자자는 개인이나 기업에 돈을 빌려주고 이자를 받습니다.

- 예: FundingCircle, Zopa

- 기부 기반 크라우드펀딩 (Donation-based Crowdfunding)

- 기부자는 재정적 보상 없이 프로젝트나 원인에 기부합니다.

- 예: GoFundMe, JustGiving

• Know some of the market leaders in the crowdfunding space.

Market Leaders in the Crowdfunding Space

- Kickstarter

- Leading platform for reward-based crowdfunding, focusing on creative projects.

- Indiegogo

- Another major player in reward-based crowdfunding, known for its flexible funding options.

- GoFundMe

- Dominates the donation-based crowdfunding market, primarily for personal and charitable causes.

- Seedrs and Crowdcube

- Prominent equity-based crowdfunding platforms in the UK, allowing investors to buy shares in startups and growth companies.

- FundingCircle

- A leader in debt-based crowdfunding, providing loans to small and medium-sized businesses.

크라우드펀딩 시장의 주요 리더

- Kickstarter

- 창의적인 프로젝트에 중점을 둔 보상 기반 크라우드펀딩의 선두 플랫폼.

- Indiegogo

- 유연한 자금 옵션으로 유명한 또 다른 보상 기반 크라우드펀딩 주요 플랫폼.

- GoFundMe

- 주로 개인 및 자선 목적의 기부 기반 크라우드펀딩 시장을 지배.

- Seedrs와 Crowdcube

- 영국의 저명한 지분 기반 크라우드펀딩 플랫폼으로, 스타트업과 성장 기업의 주식을 구매할 수 있음.

- FundingCircle

- 중소기업에 대출을 제공하는 채권 기반 크라우드펀딩의 선두주자.

• Understand different types of platform models.

Different Types of Platform Models

- Direct Model

- Investors directly own shares in the company they invest in.

- Example: Crowdcube

- Nominee Model

- A platform acts as a nominee shareholder on behalf of the investors.

- Example: Seedrs

- Coinvestment Model

- The platform co-invests alongside other major investors, providing a layer of due diligence and shared risk.

- Example: SyndicateRoom

다양한 플랫폼 모델

- 직접 모델 (Direct Model)

- 투자자가 투자한 회사의 주식을 직접 소유합니다.

- 예: Crowdcube

- 명목 모델 (Nominee Model)

- 플랫폼이 투자자를 대신하여 주식을 소유합니다.

- 예: Seedrs

- 공동 투자 모델 (Coinvestment Model)

- 플랫폼이 다른 주요 투자자와 함께 투자를 진행하며, 실사와 리스크를 공유합니다.

- 예: SyndicateRoom

• Understand governance issues related to (equity) crowdfunding.

Governance Issues Related to Equity Crowdfunding

- Adverse Selection

- The risk of attracting low-quality ventures due to less rigorous screening processes.

- Quality of Platform Screening

- The effectiveness of due diligence conducted by the crowdfunding platform. Platforms like Kickstarter are known to have stricter screening processes compared to others like Indiegogo.

- Post-Funding Governance

- Monitoring and supporting entrepreneurs after they have received funding. This can vary based on the platform model (Direct, Nominee, Coinvestment).

- Fraud Prediction and Prevention

- Ensuring that fraudulent campaigns are identified and prevented. Factors include the entrepreneur's characteristics, social media presence, campaign structure, and description.

지분 크라우드펀딩 관련 거버넌스 문제

- 역선택 (Adverse Selection)

- 엄격하지 않은 심사 과정으로 인해 저품질의 벤처가 유입될 위험이 있습니다.

- 플랫폼 심사의 품질 (Quality of Platform Screening)

- 크라우드펀딩 플랫폼이 수행하는 실사의 효과성.

- Kickstarter는 Indiegogo보다 엄격한 심사 절차를 가지고 있음.

- 자금 조달 후 거버넌스 (Post-Funding Governance)

- 자금 조달 후 기업가를 모니터링하고 지원하는 문제. 플랫폼 모델(직접, 명목, 공동 투자)에 따라 다를 수 있음.

- 사기 예측 및 예방 (Fraud Prediction and Prevention)

- 사기 캠페인을 식별하고 예방하기 위한 조치. 이는 기업가의 특성, 소셜 미디어 친화도, 캠페인 구조 및 설명 등과 관련됨.

Quiz

1. One of the mining strategies to overcome barriers to entry for most solo miners has been to do cloud mining. In cloud mining, the miner: B

A. Cannot win because computing power is idle.

B. Uses background computing power that would otherwise be idle.

C. Joins mining pools similar to lottery pools.

D. Forms a syndicate with other miners.

E. None of the above.

2. Which of the following statements most accurately describes the nominee model offered by some equity crowdfunding platforms: C

A. Investors make direct investments and must monitor themselves.

B. Only B-shares are offered so that investors do not have to monitor.

C. The platform acts as a trustee and is doing the monitoring for the crowdinvestors.

D. Crowdinvestors invest along side angel investors and venture capitalists.

E. None of the above.

3. Which of the following statements most accurately represents facts we learned from the OakNorth presentation today? OakNorth… E

A. Focuses on the largest businesses that grow slowly but have stable cash flows.

B. Is listed on the London Stock Exchange through it can issue additional equity.

C. Owns its Credit Intelligence Suite that monitors the business climate.

D. ‘s acquisition of SVB will prevent bank runs in the future.

E. has a simple product portfolio consisting of business loans and personal savings.

4. In rewards-based crowdfunding, which of the following most accurately defines AON or KIA? E

A. AON means “All onboard”, which occurs when every investor has provided capital.

B. AON means “All-or-nothing”, i.e., all capital received, but no shares issued.

C. KIA means “Keep-it-aside”, i.e. entrepreneurs should not spend all capital at once.

D. KIA means “Keep-it-all”, i.e. entrepreneurs can keep the raised capital when above target.

E. KIA means “Keep-it-all”, i.e. entrepreneurs keep the raised capital even if below target.

5. What are some of the advantages for entrepreneurs when raising capital through rewards-based crowdfunding? C

A. The early dissemination of information on the platform can increase competition.

B. Entrepreneurs need to hire more public relations personal to collect all the feedback.

C. There is no dilution in control.

D. Entrepreneurs can access VC funding cheaper, but also need to pay their crowdfunders.

E. None of the above.

Instagram: subin_102426

'👩🎓𝐒𝐓𝐔𝐃𝐘 > Fintech & Blockchain' 카테고리의 다른 글

| Practical Lecture 6: Deep Learning (1) | 2024.07.03 |

|---|---|

| Lec 7: Initial Coin Offering [ICOs] (1) | 2024.07.03 |

| Lec 5: Altcoins / 알트코인이란? (0) | 2024.03.09 |

| Practical Lecture 3: Mining Technology and Industry (2) | 2024.02.24 |

| Lecture 4: Blockchain Governance / 비트코인 한계점 & 하드포크란? (0) | 2024.02.23 |